Endowments Poised to Build on Recovery, Chronicle Study Finds

By Ben Gose and Marisa López-rivera

May 30, 2011 | Read Time: 8 minutes

The nation’s charity and foundation endowments appear to be on the path toward a prosperous 2011, after earning strong returns in 2010, according to a new Chronicle survey.

The survey of 213 organizations found that endowments of all sizes earned median returns of 12 to 13 percent in 2010. More than two-thirds of the endowments reported their year-to-date performance for 2011, and they have earned a median return of 8.3 percent so far this year, meaning that half are doing better than that and half are faring worse.

The total value of the 213 endowments that provided data for both 2009 and 2010 was $340.2-billion in 2010, a gain of $27.2-billion.

The Chronicle’s findings mirror those of a survey of 175 foundation endowments released last week by the Commonfund Institute. Foundations in that survey achieved returns of 12.5 percent last year (compared with 20.9 percent in 2009), while 69 charity and operating-foundation endowments examined in a separate Commonfund study increased returns by nearly 12 percent last year, compared with 21.5 percent in 2009.

Small but Strong

Smaller endowments outperformed their larger counterparts for the first time in many years in 2009, and in 2010, the smaller endowments held their own once again, largely by sticking with stocks and other depressed assets that continued their rebound following the financial crisis.

City Year, the youth-service corps with headquarters in Boston, earned a 22-percent investment return on its $7.5-million endowment in 2010, in part due to its aggressive 85-percent allocation to stocks at the beginning of its fiscal year in July 2009. (The endowment changed investment managers in February and now holds more-diverse assets.)

The charity did not spend any of its endowment in 2010, to allow the modest-size pool to continue to build, says Evelyn Barnes, City Year’s chief financial officer.

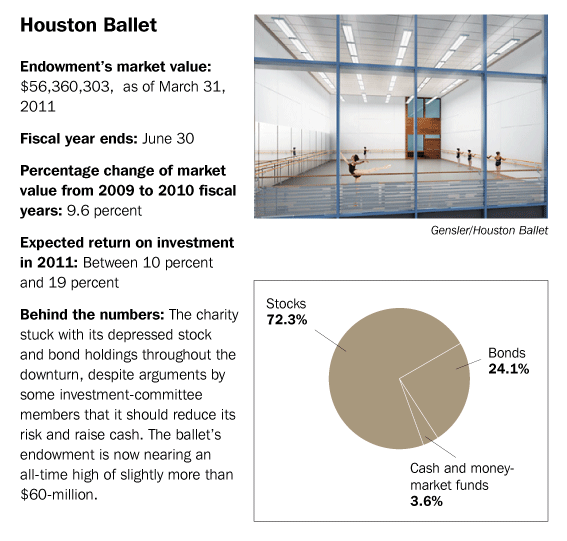

Houston Ballet’s $56.4-million endowment also did well, earning a return of 16.8 percent for its fiscal year ending in June 2010.

Cheryl Zane, the charity’s finance director, says the ballet stayed invested in bond holdings that had dropped sharply during the financial crisis, despite arguments by some board members that the endowment should sell the bonds to raise cash. The charity has some other big financial commitments, including $4-million in debt on its new $46-million Center for Dance.

But Ms. Zane says the managers of the bond funds visited the charity several times to argue that the bonds were only temporarily depressed. “We felt that they would turn around,” she says, “and we were rewarded by staying.”

Souring on Stocks

While the best-performing endowments stuck with stocks in 2010, endowments as a group are gradually cutting their allocations to stocks, in part because some investment managers still bear scars from the financial crisis in 2008 and 2009. They worry about disappointing not just the nonprofits that depend on them for money to run programs but also the donors who support their causes.

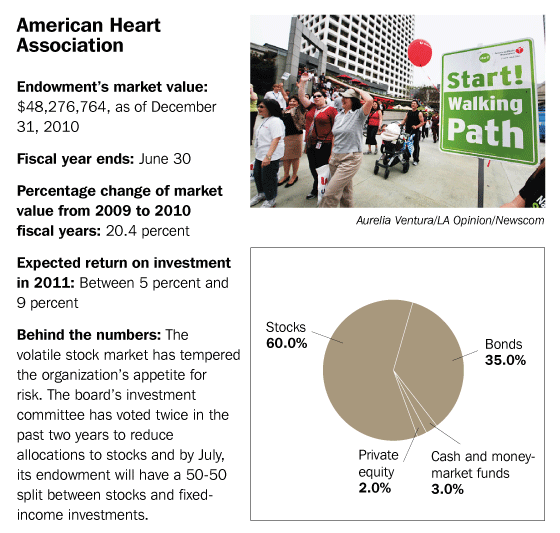

The American Heart Association, which has a $48.3-million endowment and another $350-million in operating reserves, saw its investments drop 11 percent in 2008 and 16 percent in 2009, before bouncing back with a 12.1-percent gain last year.

In June 2009, the board’s investment committee voted to cut the endowment’s allocation to stocks from 75 percent to 60 percent and lift fixed income from 25 percent to 40 percent.

This February, the investment committee cut stocks even further, voting for a 50-50 split between the two asset types.

“Our risk appetite has gone down,” says Sunder D. Joshi, the Dallas organization’s chief financial officer.

He says the changes were motivated not only by a desire to avoid losses but also by how such declines might be perceived by donors. “The concern was about losing a lot of the money that donors are giving us to fight the fight,” Mr. Joshi says.

Appeasing Supporters

Many other nonprofits are also cutting back on stocks, The Chronicle study found when it examined trends for the 106 organizations for which it has five years of data.

Those groups had a median of 43 percent of assets in stocks during 2010. Four years earlier, in 2006, the same group had a median of nearly 55 percent of their assets in the stocks.

But investment committees should think twice before making major changes, some advisers say, particularly if part of the goal is to appease supporters worried about market volatility.

“If the markets do well, you’ll have the same people pointing fingers and saying, ‘Why are you in the bottom quartile of returns?’” says Sarah Stein, a managing director of Hall Capital Partners, an investment firm that oversees $22.4-billion, including a few billion for endowments and foundations.

Managers may be obsessing too much about short-term performance, leading them to unload investments too quickly, some studies suggest.

A 2009 survey of 111 investment-committee members by the Vanguard Group, the mutual-fund company, found that investment committees spend 40 percent of their time evaluating past performance, far more time than they spend on activities that they have greater control over, such as evaluating investment costs and allocating assets.

“People are spending way too much time on the minutiae of investment performance,” says Catherine Gordon, who heads Vanguard’s institutional asset-management group.

Yet Hall Capital and other investment advisers say regular tweaks are important, and they are encouraging charities and foundations to put their endowments in a position to defend against two very different threats—another downturn and high inflation.

One strategy for navigating another downturn is to create a pool of safe and liquid investments within the endowment that could be used to cover a charity’s operating expenses for six months or a year. The strategy could help charities avoid having to unload stocks at fire-sale prices—a reality that ensnared some endowments during the financial crisis. Some organizations, meanwhile, are considering pulling unrestricted assets out of their endowment to eliminate debt.

Hedging Bets

Endowments can avoid the worst of a stock-market decline by building a bond portfolio in which individual bonds mature at regular intervals, providing cash the nonprofit needs to help finance its programs. Certain types of hedge funds, which try to earn a positive return in both rising and declining markets, also can ease the pain when stocks swoon.

The Los Angeles County Museum of Art began considering a move into less volatile investments in the summer of 2008—but it wasn’t able to carry out its plan until 2009, after the markets dropped. The museum’s $120-million endowment saw its investments fall 7 percent in 2008 and 23.4 percent in 2009.

“If only we had done it six months earlier,” says Michael Govan, the museum’s director.

The charity now keeps half its assets in hedge funds designed to be less volatile than the stock market. The museum’s stock allocation is just 21 percent, down from more than 50 percent before the financial crisis hit. Despite the more-conservative allocation, the endowment earned an above-average 13.6-percent return in 2010.

Solid-Gold Investments

To protect an endowment against inflation, experts recommend inflation-adjusted Treasury bonds, real estate, and commodities like gold, oil, and timber.

The Chronicle’s survey suggests that endowments may be following such paths. The share of assets dedicated to hedge funds and “other” (which includes commodities) rose sharply over the past five years.

The University of Texas Investment Management Company, which manages endowments worth nearly $20-billion for the University of Texas and Texas A&M systems, reported in April that it is holding about $1-billion in gold, in the form of actual bars of bullion.

The prices of commodities like gold and silver have spiked in recent years. John Paul Cavaliere, a senior analyst specializing in nonprofit advice at SEI, an investment management company, cautions that endowments should add commodities for diversification, not because they’ve been a hot investment.

“You bring these assets in for a specific purpose—because they will do well in a rising interest-rate environment,” Mr. Cavaliere says. “But you have to be willing to accept the downside risk that they bring.”

Raising Money

Some charities with the biggest percentage increases in market value relied on fund raising, rather than investment return, for their growth.

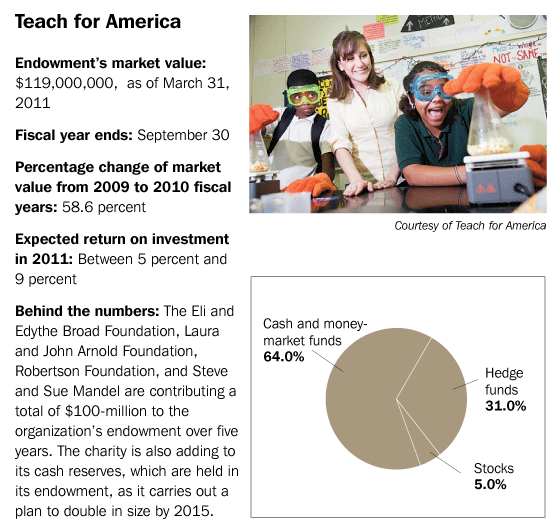

For example, Teach for America’s $119-million endowment has tripled in less than three years, and it will continue to expand, thanks to four grant makers, led by the Eli and Edythe Broad Foundation, that have pledged to put $100-million into the endowment over five years.

The New York charity plans to hold off on spending from the endowment for at least a few more years, says Beth Anderson, senior vice president for national development. Teach for America is hoping to double its size by 2015.

“The bigger we can grow the endowment, the more meaningful its size will be as our organization gets to a larger scale,” Ms. Anderson says.

Rainy Days

One key reason for maintaining an endowment is to help the nonprofit survive hardships—and that applies to one of the biggest losers in the survey.

The Nashville Symphony Association’s endowment stands at $55.4-million, down from $72.2-million last July. The May 2010 floods that hit Nashville caused $40-million of damage to the symphony’s concert hall.

Insurance provided $10-million, and federal disaster assistance will ultimately cover $25-million more. But a year after the disaster, the charity is still waiting to receive more than half the federal money, according to Alan Valentine, the symphony’s president.

While water was still flowing into the basement, the symphony’s board voted to borrow $18-million from the endowment to get repair work under way. The quick decision allowed the hall to reopen by January 1 for a special concert with Itzhak Perlman. The endowment will be repaid when the federal disaster funds arrive.

“If anybody ever questions why a nonprofit needs an endowment,” Mr. Valentine says, “I can tell them why.”

Peter Bolton contributed to this article.