Investment Beliefs: Government Bedrock for Investment Committees

How to Build Resilience into an Investment Process for Perpetual Portfolios

October 8, 2019 | Read Time: 9 minutes

Where to Start? Recognizing the Proper Role of Governance

An effective investment governance process aligns an institution’s ability and willingness to make investment decisions with the long-term needs of its portfolio. The governance process itself can be as difficult to establish as constructing a sophisticated investment portfolio, because every institution has unique capabilities, objectives, needs and preferences. Ultimately, we believe institutions should strive for a governance process that achieves three goals:

- An organization that relentlessly focuses on its long-term vision.

- A governing board that confidently supports the investment strategy.

- An investment committee that steadfastly implements an investment strategy based on sound investment beliefs.

Get in the Right Mindset! The Process for Developing the Investment Beliefs Document

- Control personal biases, especially if they are overly centered on mitigating short-term risks at the expense of any long-term rewards. It often helps to view risk-bearing capacity and return objectives through the eyes of the organization’s mission, needs, and longevity.

- Rely on experts and successful investors for guidance. Investment beliefs shouldbe a product of careful, thoughtful analysis and the collective experiences and insight from not only committee members but also industry experts.

- Address six key questions to develop a set of coherent and consistent investment beliefs. (Fear not! It can be a mission-affirming and enriching process.)

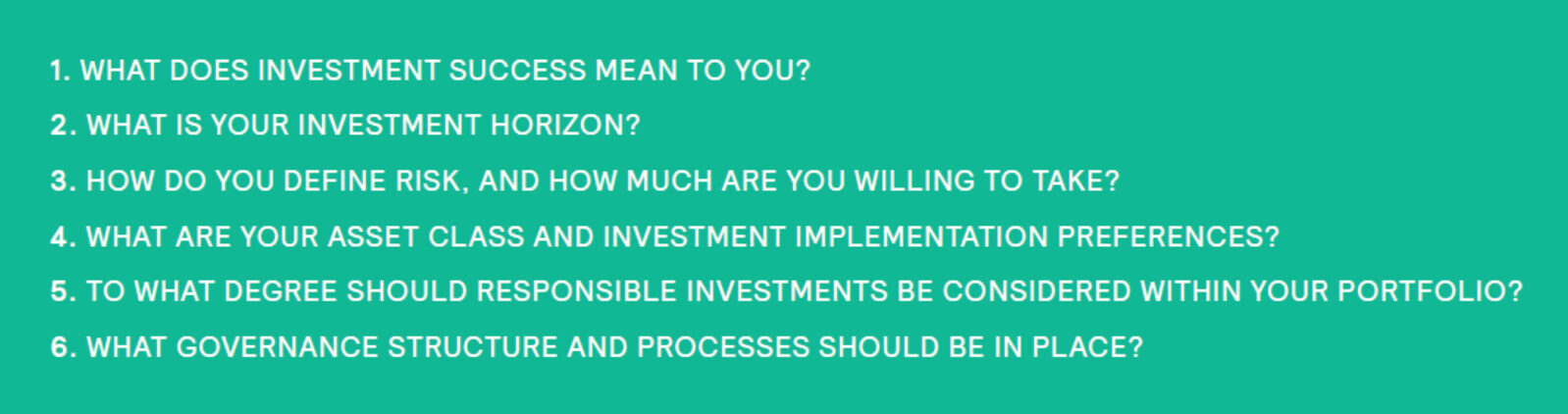

SIX KEY QUESTIONS FOR DEVELOPING INVESTMENT BELIEFS

Investment beliefs can cover a broad swath of issues and each set of beliefs should be customized to your organization, committee, and objectives. Pavilion’s experience helping investment committees develop their belief statements has led us to focus on six key questions:

1. What Does Investment Success Mean To You?

Although investment success varies from organization to organization, there are typically three approaches to measuring it:

- absolute performance relative to a specific goal in order to preserve intergenerational equity;

- performance relative to the investment policy benchmark; and

- performance relative to peers.

These measures are useful in different ways, so prioritizing them is critical.

2. What Is Your Investment Horizon?

Most organizations have a stated investment horizon as well as an unstated, and often much shorter, “patience horizon.” (The shorter horizon sometimes reflects the tenure of committee members who only serve for a limited time.) The question for your organization is whether these stated beliefs can be sustained through periods of short-term underperformance in pursuit of longer-term opportunities. In other words, can you stay focused, patient and disciplined and ignore the temptations of a “patience horizon.”

3. How Do You Define Risk, And How Much Are You Willing To Take?

There are myriad definitions of risk that affect all institutional investors. They include purchasing-power risk, illiquidity risk, headline risk, market value and distribution volatility, peer-relative risk, risk of steep losses, etc. An investment committee should articulate the most relevant risks for the institution, rank them, and decide which ones should be measured and mitigated and which ones should be ignored or even embraced in the perpetual portfolio. The discussion should include:

How much liquidity do you really need?

Every organization needs a stream of income for short-term needs. But it is just as important to decide how much to put in medium-term and long-term liquidity buckets — we think of it as “the money you can get to, the money you plan for, and the money you can’t touch.” Most endowments and foundations have assets that will not be used for years, or even generations, and fail to capitalize on this untapped resource for funds that can be placed in longer-term investments with higher return potential.

How big a market drop can you really weather?

It is vital to anticipate how the portfolio — and the investment committee — will respondto inevitable market shocks. During volatile periods, when institutional and individual investors are more likely to see steeper declines, they experience what behaviorists call “myopic loss aversion.” The more they look at their portfolios, the more pain they feel,and the more apt they are to react to recent losses — possibly at the expense of long-term benefits.

The key question is how much short-term turbulence the organization can accept in pursuit of higher returns over the long term. For example, in one year out of ten, could the institution sustain a 20% loss over a rolling 12-month period? If not, the investment committee should consider some allocation to safer, less aggressive investments. A “risk/response” guideline statement, written during periods of relative market calm, can establish a clear set of rules under which to take action, or even no action, in the interest of long-term investment success.

4. What Are Your Asset Class And Investment Implementation Preferences?

Every investor has asset class preferences and biases. A complete set of investment beliefs spells out the rationale for the long-term investment portfolio structure and discourages short-term changes due to whims or what is hot in the investment world at the time. Only fundamental economic shifts or secular changes in market structure should lead to changing preferences of, and within, asset classes. Implementation preferences usually take the form of decisions around active vs. passive investments, traditional assets vs. alternatives, growth vs. value, market capitalization (large vs. small), and US vs. non-US exposures. Preferences also include which vehicles can (or cannot) be used, such as separate accounts or private partnerships.

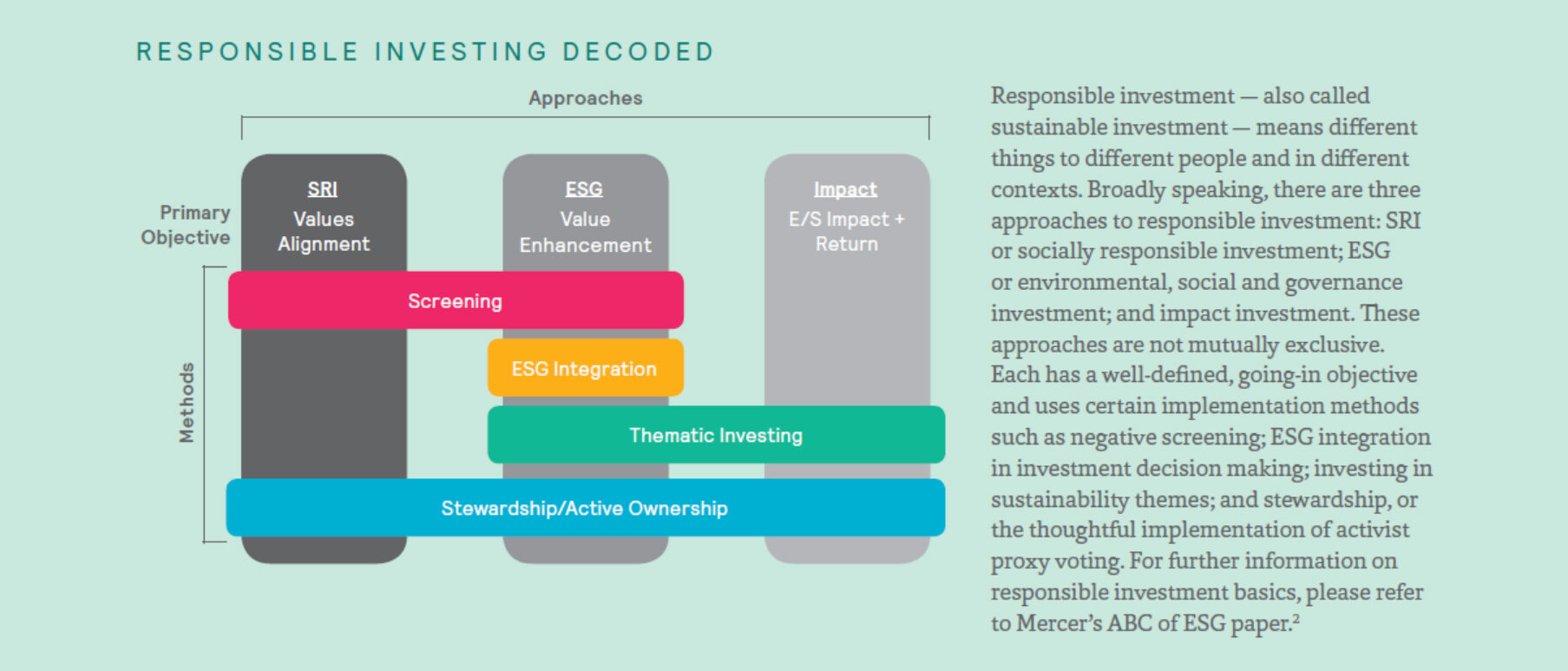

5. To What Degree Should Responsible Investments Be Considered Within Your Portfolio?

A number of institutions, particularly foundations with mission-driven roots, naturally gravitate toward responsible investing, which involves the consideration of ESG (environmental, social and governance) factors in investment portfolios. Key questions typically arise around whether, how and how much to orient the portfolio toward such factors. The beliefs statement should provide a blueprint for the responsible investment approach to be adopted and to what degree.

6. What Governance Structure And Processes Should Be In Place?

Formulating a good governance process includes addressing such questions as:

- Does your governance structure align with a long-term investment horizon?

- How qualified is the investment committee to make investment decisions?

- Is the committee receptive to education on the issues that will come before them?

- Does the committee support and encourage transparency?

- Has the committee asked for reporting that is appropriately focused on bothlong-term success as well as the short-term issues?

- Are there structures and processes in place to achieve the institution’s investment goals?

- Are there policies in place to maintain consistency in the face of turnover in staff, board, or investment committee members?

ACHIEVING CONSENSUS ON YOUR ORGANIZATION’S INVESTMENT BELIEFS

There is no “one size fits all” formulation of investment beliefs; even ostensibly similar organizations may have very different sets of priorities. But codifying beliefs in an investment policy statement is critical to ensuring continuity of organizational mission, purpose, and governance. And once established, investment beliefs should become bedrock guiding principles, ones that should be regularly reviewed but rarely changed. While having an explicit statement of investment beliefs can lead to better investment decision making, more importantly, it can lead to better investment outcomes.

CASE STUDY: ESTABLISHING A BEDROCK FOR YOUR ORGANIZATION

Background/Client Profile

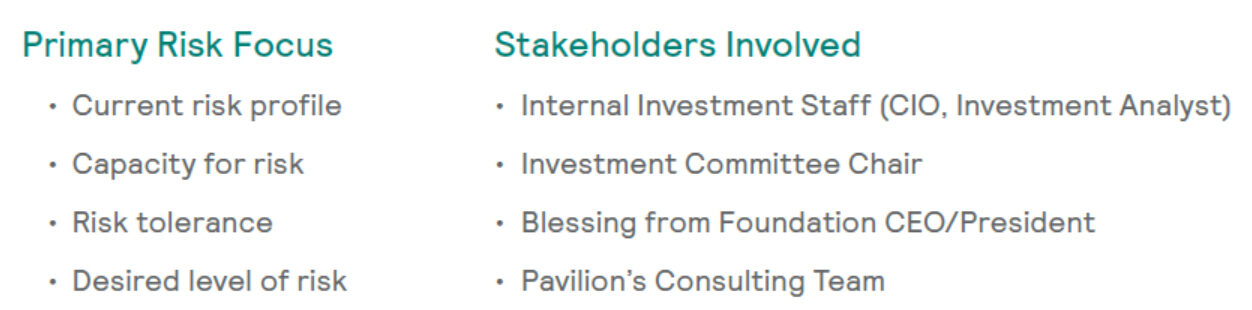

A large public foundation has one investment portfolio of approximately $800 millionin assets. Its broadly defined mission is to support neuroscience services globally. The foundation’s board delegated the development of the investment policy statement and its execution to an investment committee comprised of 12 volunteer members, along with the foundation’s CEO/President. The committee has wide-ranging backgrounds but a common philanthropic mindset. Given significant growth over the last decade, the foundation decided five years ago to begin building its own internal investment team, hiring a Chief Investment Officer and Investment Analyst.

Challenge

Overseen by two strong and opinionated chairpersons over the past ten years, the investment portfolio reflected each individual’s general investment preferences during each of their respective tenures. With two massive directional changes in philosophy, the portfolio delivered subpar performance stemming, in part, from an alternative investments and funding methodology that was never fully embraced.

Time Horizon

Perpetual

Pavilion’s consulting team introduced the topic of developing a set of investment beliefs and worked closely with internal investment staff to refine and hone the set of beliefs for the investment committee’s approval.

Process

In recognition of impending organizational change, Pavilion advocated to secure a beliefs-based blueprint to guide portfolio decisions. Along with a comprehensive review of the foundation’s current investment program, Pavilion led an engaged discussion of its investment objectives, beliefs, governance, reporting and asset allocation policy. Along the way, many viewpoints and analyses were considered and studied.

Outcome

After a six-month process, the foundation adopted a set of 12 investment beliefs. This process resulted in several modifications to the direction of the portfolio, oversight process, and streamlined reporting that the investment committee, investment staff and Pavilion believed would enhance its performance and management.

Since adoption, the foundation’s investment beliefs have been tested many times due to episodic underperformance directly related to inherent biases deliberately implemented within the portfolio (e.g., active management, value overweight, as well as the use of private markets, which lagged during a sustained bull market). Despite these short-term challenges, the investment committee has adhered to its investment beliefs in support of the foundation’s long-term mission. As a result, there no longer is any discussion of short-term performance at committee meetings, which has allowed the committee to focus exclusively on the portfolio’s strategic direction.

HOW WE CAN HELP

If your organization is at the stage of considering drafting or clarifying its investment beliefs, here are the ways the endowment and foundationexperts at Pavilion can help:

- Conduct a survey of staff, board/committee members and other decision makers to determine their attitudes in relation to investment issues.

- Facilitate a meeting or workshop to develop, analyze, debate, and document your investment beliefs.

- Provide sample investment beliefs

- Coordinate input from management, the board, the investment committee, and investment managers to “stress test” the investment beliefs and ensure they have the potential to achieve the desired outcomes and/or understand the implications to your investment program.

- Implement the guiding principles codified in your investment beliefs to facilitate governance decisions and ensure compliance through appropriate reporting structures, meeting structures, and portfolio exposure analyses.

ABOUT PAVILION

Pavilion, a Mercer Practice (“Pavilion”) offers a full spectrumof research, advice and delegated solutions for mission driven organizations. Our diverse group of investment consulting specialists—who have deep expertise in the healthcare, endowment and foundation segments—unites in its passion to help propel your organization’s mission forward through customized solutions aimed at improving long-terminvestment outcomes. We turn our insights into actions and your goals into accomplishments. Pavilion is the Not-for-Profit consulting segment within Mercer’s Wealth division in the US. Services provided by Mercer Investments LLC. Formore information, visit www.pavilion-notforprofit.com. Follow Pavilion on LinkedIn.